I tried Experian credit boost. Does it really instantly raise your credit score?

With weeks and months of free time, I needed a hobby. I became obsessed with something everyone has — a credit score — and how I could get my score higher and higher. I did a little research for how to raise your credit score, and tried them for myself. Here’s what actually raised my credit score — and by how much.

Pop quiz: How many credit cards does the average American have?

A. 1

B. 2

C. 3

D. 4

Before I share the answer, I want to share some knowledge on how credit cards affect your credit score. For one, a credit card application can ding your credit score five points.

Closing your credit card account can also ding your score — quite significantly, if you’re not careful. But that math is a little tricky. It looks at your credit utilization and credit history length. If your utilization goes up and your history length goes down, your score takes a hit.

If you are keeping an eye on your credit score — which, by our records, many of you are — you need to know this kind of information.

Oh, and the answer you’ve been waiting for: the average American has four credit cards.

How close were you?

Anyways, in the spirit of March Madness, shall we look at the score? Credit score, that is. It is, after all, one thing we’re all quite obsessed with.

Be it a byproduct of boredom or gamification of personal finances, credit score has captured our attention. I, like a lot of you, have had extra time on my hands and no place to go. For entertainment, I found myself playing around on personal finance apps. In the early days of the pandemic, I found Robinhood. Then others followed.

With nothing to do, playing the game of finances became my newfound hobby. Apps like Robinhood made something so seemingly boring — investing — now feel like a game. With each new day, I craved a new challenge. Up until I was met with one I heartily wanted to master — my credit score.

It’s like Space Cadet 3D Pinball I used to play endlessly on my parents’ Windows PC as a kid. My eyes were stuck glued to the score. I could spend all day thinking of every way to get that score to inch higher. Being a pinball wizard was my day job. My obsession was no longer the outdated pinball game, but on an elusive score — one I’d already been given. Can I make my credit score go up? What’s everyone else’s credit score? How do I increase my credit score to 800? All were questions I pondered as I jumped with both feet into my new obsession.

Yes, I found a way to boost my credit score. You can raise your credit score, too. But I encourage you to read on, as it’s not as simple as unlocking the extra ball in Space Cadet 3D Pinball.

Jump ahead:

How I increased my credit limit.

What Experian Boost did to my credit.

Why I’m stuck at the same credit score.

How to borrow money with bad credit.

In the days of Space Cadet 3D Pinball, there were no hacks — at least none that anyone told me about. But with credit score, how to hack your credit score returns infinite search results. Anyone from novices to beginners can hack a credit score for the better, so they say.

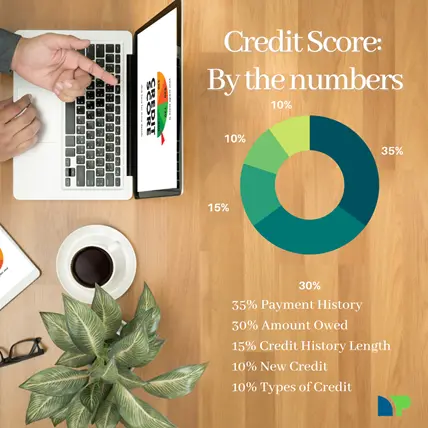

How exactly? Turns out the secret to playing the game is understanding how the game is scored. For reference, I’ve put together a chart below that breaks down the math behind a FICO credit score.

What determines my credit score?

Scoring metrics in mind, it’s easier to game plan how you want to play. Most people know the basic ideas of building good credit scores. But even when I was assembling my own strategy, I found too many suggested hacks to better my score. I couldn’t simply try them all — at least not all at once.

I was already paying on-time. I started paying early

With the math laid out in front of me, I began to strategize. I already was paying my bills on-time, so I could check off the first box. But what about the amount owed? It is pretty clear that maxing out credit cards is a generally negative credit score catalyst. How could I do better here?

I had become used to waiting for my credit card bill to come, then paying it a day or two after. But I stopped paying my credit card bills once a month. Instead, I made a habit of paying my credit card balance every Friday.

Why? Credit utilization is why. By consistently paying down my account balance, I was able to keep my utilization below 10% pretty much all the time. Whereas had I waited and paid all at once, my utilization may spring upwards of 25% or more. Frequent payments help me to shrink my utilization ratio, and send my score on an upward trajectory.

I knew that if I messed up, I could ask for forgiveness

It’s not easy to be on-time. In fact, I’m usually late. My definition of “I’m on my way” means I’ll get out of bed in 5 or 10 minutes and hit the road in 20ish. Though I try not to, I may let my tardy tendencies slide over into my bills, resulting in a missed payment. Fair warning: a “I’ll be there in 5” text to the credit card company doesn’t land well.

Missing a payment hurts. They may hit you with a late fee and penalty APR, even if only a day or two late. And if you happen to lapse a billing cycle, it could drop your credit score up to 100 points. Seriously, ouch.

There is, thankfully, a solution to a missed payment. It starts with taking responsibility for the missed payment and offering to pay it now. Take care of that, then it’s fair game to ask them to remove the late payment from your credit score. You may have to write a letter of goodwill to fully resolve the issue and get your credit score back on track. I can’t guarantee your issuer will go for this, but they might. Oh, and btw, if they do spring for this, know this is kind of a one-time deal.

Then I increased my credit limit

How about adding another credit card? Turns out, that’s not a terrible idea. Already, I kept two credit cards. By adding a third, I could increase my credit limit and spread out my spending among the three cards instead of two. Collectively, my amounts owed, relative to my credit limit, would go down. And fingers crossed, my credit score would go up.

On top of adding a third card, I also asked my creditors to increase my credit limits. Increasing my available credit was something I was able to do in a few short minutes over the phone. In one case, I was able to apply for an increase online. It wasn’t hard to get approved, seeing as I had a track record of paying on-time and hadn’t maxed out my account before. My creditors willfully obliged.

How low should you go? Experts suggest to keep your credit utilization under 25%. But even better is under 10%. Another plus, I learned, is to not cancel a credit card account. Why, exactly? Two reasons. First, should you cancel an existing credit card account, your available credit will decrease, and subsequently, your utilization will go up. Second, should you cancel a long-term account, your credit history length will decrease, and likewise drop your score. Even if not using the account, simply keeping it open can be a plus.

Next, I called in reinforcements

By this point, I had done quite a bit of work and to see my credit score hardly budge. These hacks, really could only do so much. But, as you might guess, I had free time on my hands and wanted to see what more I could do to help nudge my score — even if a point or two. So I called my landlord.

Thanks for a new rule, my on-time rent payments can now be included in my credit score. It’s up to your landlord to decide whether to report your on-time payments. With a little persuading, I was able to get her to agree to report my on-time rent payments.

Then I signed up for Experian Boost. It suggests it can raise your FICO score instantly. What did I have to lose? Experian Boost, I learned, looks for on-time payments for routine monthly expenses, and adds them to your report. Things not looked at, like utility bills, cell phone bills, and streaming services (hint, hint: your Netflix account), would be counted now.

It worked, and raised my FICO score six points. Average users, Experian says, improve their score by eight points, and in some events by 13 points. Nonetheless, six points is six points. It worked.

I thought to have a look at my credit report

My parents taught me two important things: people make mistakes, and always pay attention to detail. With that in mind, I haven’t exactly been shy to point out mistakes.

I can’t promise my teachers much appreciated this, if I were to point out a mistake on an assignment or test, or a grading error. Although not always met with appreciation, my pointing out a mistake was always accepted.

Like that of a report card, I thought I might check my adult report card. I’m referring to my credit report. It should list my account history, any hard credit inquiries, and otherwise public records. It was worth me taking a few minutes to check through to make sure everything was all good, operating as my own checks and balances system.

In a couple of minutes, I was able to check for any incorrect records or accounts listed in my report. Fortunately, everything checked out nicely, with nothing misreported. Others I know weren’t as fortunate, and had incorrect information in their report. Turns out that’s somewhat common — 17% of credit reporting complaints concern incorrect information.

In some cases, it may be the result of a name mix up or harmful identity theft. In either case, resolving the issue is easier than you think. Most credit agencies have set up fraud protection and can put a fraud alert on your account in minutes. Altogether, I’m more confident that my credit score reflects the real me after ensuring only the right information was included in my credit report.

Why I’m stuck at the same credit score

For weeks and months, raising my credit score has been my hobby of choice. In the early days of my journey, I had a lot of positive movement. Then, things slowed down. Picture a car meeting holiday traffic on Interstate 405. Yep, that slow. If you’re wondering what movement my score has made of late, it’s still trapped between the sedan and pickup that have hardly moved in the last half-hour.

What gives? Well, let’s just say age isn’t just a number in the eyes of credit bureaus. Older accounts look better and fare a better score. My accounts are still fresh and young. They need time to age before my credit score will go up any higher.

Too, the higher your credit score gets, the harder it is to keep increasing it. Kind of like rock climbing, the initial descent is fairly easy and happens quickly. But the final half is much more challenging on your tired body and takes a while. When your score is in the 500s or 600s, you can increase it by simply not doing wrong. Making progress with a score in the 700s is a much slower process.

Breaking into the 800s requires that you don’t borrow too much and pay your bills on-time — for a long time. How long is a long time? Hate to break it to you, but a score of 800 or higher requires 10 years of positive credit history. I hacked my credit score about as far as I can for now. About now, all I can do is stay consistent and wait.

Does credit score matter all that much?

It’s about this time I could hear my parents telling me to stop playing Space Cadet 3D Pinball and go play outside. I obsessed over my credit score like I was watching the grass grow. Yes, I can tirelessly work on getting my credit score as high as possible. But is it worth my time? Not even.

If you believe everything you read about credit score, you’d think it was the single-most important thing in your life. It’s not. This isn’t to say that credit scores don’t matter and you shouldn’t waste your time. A credit score does hold value. You can leverage a good credit score into better deals on loans, credit cards, and insurance premiums. Low credit scores will cause a loan to be approved at a higher rate, that, over a lifetime are quite pricey.

For example, someone with a 620 FICO score would pay $65,000 more on a $200,000 mortgage than someone with a 760 FICO score. If you have a good credit score, you’ll almost always qualify for the best interest rates, and pay less — which I’m sure is something you want.

While that is true, credit score doesn’t tell the whole story. All a credit score tells you is if you are good at borrowing money and paying it back. That’s really it.

A lot of people say they want to get a perfect credit score, but few actually achieve it. The good news is that no one actually needs an 850 score to be seen by lenders as having good credit. Often a 760 score is enough to qualify for the best lending terms.

You know what you get for a 800 FICO score? Or 850? Honestly, not a lot more. No bank has a product exclusive to someone with an 850 credit score. If they did, they’d be canceling out about 99.5% of the market. To be clear, most banks offer the best-published interest rates to anyone with a 760 credit score or better.

Trying to micromanage your credit and stressing about it could cause you to make bad decisions. Obsessing over your credit score will surely lead you to more headaches, because the math is complex and the numbers don’t always add up. Instead, the healthiest thing you can do is keep up your good habits and let your score be.

Your credit score is like an adult report card. Sure, every kid would love to have a perfect report card hanging on the fridge. I’m sure every adult would love to have perfect credit, as well. But that’s not reality — and that’s OK.

How to borrow with a bad credit score

For most financial institutions, loan decisions are decided by a borrower’s credit score. But what if you’re still working on your score and had a hiccup or two along the way?

Some lenders offer short-term personal loan assistance with no hard credit check required. Net Pay Advance is one that supports individuals with no-credit-needed payday loans. We run a soft credit inquiry to verify information and assesses a loan decision instantly.

Net Pay Advance lends you up to a few hundred dollars, depending on eligibility, and delivers straight to your checking account. Most customers have their money deposited the next day. Eligibility is dependent on a few factors, including location, account history, and deposit frequency — but not your credit score.

Learn more about securing a no-credit-check personal loan here.

Disclaimer: Above, I have highlighted some ways I personally raised my credit score. These suggestions may not be applicable to everyone, and may not fit your financial picture. Please exercise caution should you use these tips. Results of a better credit score are not guaranteed.